Fed Rates: What They Are, Why They Matter, And How They Impact Your Wallet

Let’s cut to the chase, folks. Fed rates—or Federal Reserve interest rates—are one of those terms that get thrown around in financial circles all the time. But do you really know what they mean? If you’re scratching your head right now, don’t sweat it. You’re not alone. Fed rates play a massive role in shaping the economy, affecting everything from your mortgage payments to the cost of that morning latte. So, buckle up because we’re diving deep into this financial beast.

Think of the Fed rates as the heartbeat of the U.S. economy. They’re set by the Federal Reserve, which is basically the central bank of the United States. These rates determine how much it costs for banks to borrow money from each other. And guess what? That cost trickles down to you, the everyday consumer. Whether you’re saving, spending, or borrowing, fed rates have a say in how much you’re paying or earning.

Now, if you’re wondering why you should care about fed rates, let me break it down. They influence inflation, employment rates, and even global markets. In simpler terms, they affect your wallet. If the Fed decides to raise rates, borrowing becomes more expensive, which can slow down spending. On the flip side, lower rates can stimulate the economy by making loans cheaper. So, yeah, you better pay attention because your financial future depends on it.

What Exactly Are Fed Rates?

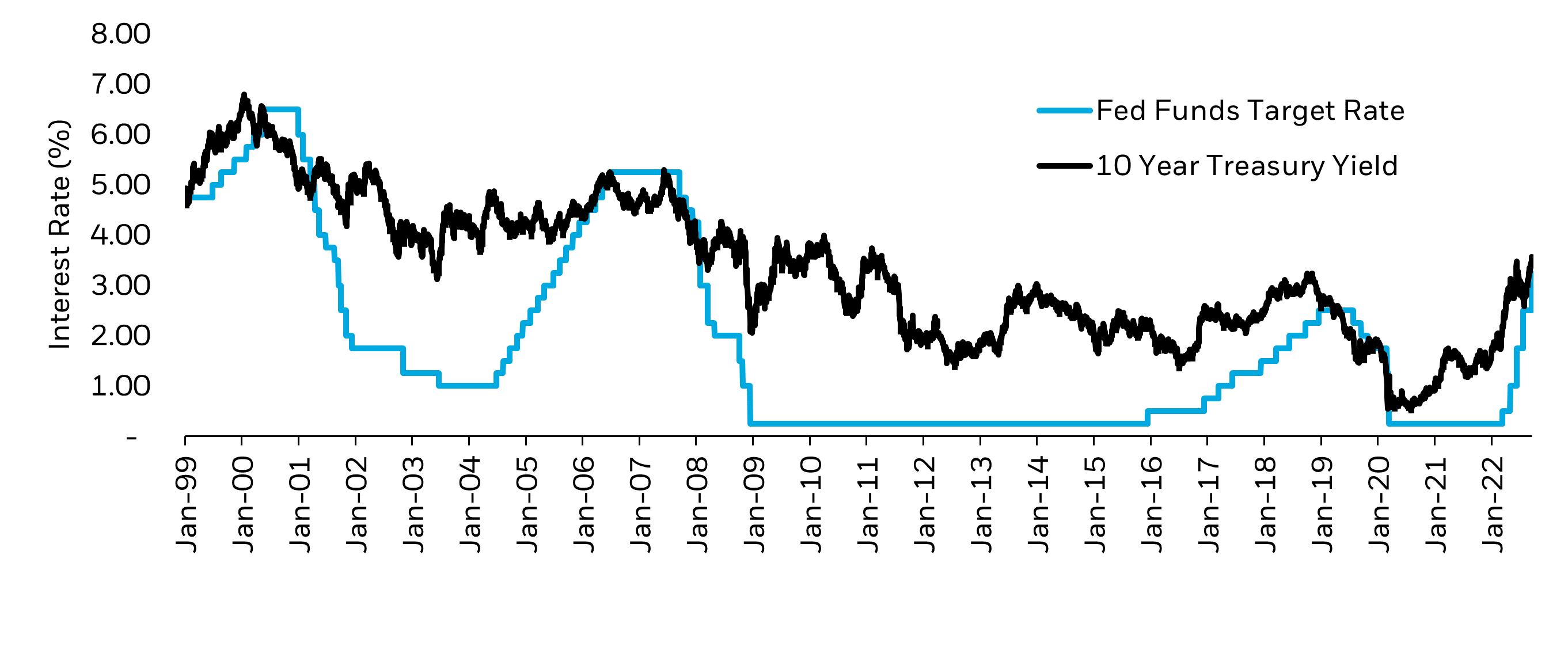

Fed rates, also known as the federal funds rate, are the interest rates at which banks lend reserve balances to other banks overnight. This is how banks manage their liquidity and ensure they meet their reserve requirements. The Federal Reserve sets a target range for these rates, and it’s a big deal because it sets the tone for the entire financial system.

Let’s break it down further. When the Fed lowers rates, it’s like turning on the spigot for economic growth. Businesses can borrow money more easily to expand, and consumers can take out loans for big purchases like homes and cars. But when rates go up, it’s like slamming the brakes. Borrowing gets pricier, which can slow down spending and help control inflation.

Why Should You Care About Fed Rates?

Here’s the thing: fed rates aren’t just some abstract concept that economists talk about. They hit close to home. If you have a credit card, a mortgage, or a student loan, the interest you pay on those is directly tied to fed rates. For example, when the Fed raises rates, your credit card APR might go up. That means you’ll pay more in interest if you carry a balance. Not exactly pocket change, right?

On the flip side, savers benefit when rates rise because they earn more on their savings accounts and certificates of deposit (CDs). So, if you’re the type who likes to stash cash in the bank, higher fed rates could be your best friend. But if you’re a spender or a borrower, you might want to reconsider your financial moves when rates are climbing.

How Do Fed Rates Affect the Economy?

The impact of fed rates on the economy is like a ripple effect. When the Fed lowers rates, it’s usually to stimulate growth. Businesses invest more, consumers spend more, and the economy gets a boost. But if the economy overheats and inflation starts to rise, the Fed steps in to cool things down by raising rates. It’s a delicate balancing act, and the Fed has to be strategic about its moves.

For instance, during the Great Recession of 2008, the Fed slashed rates to near-zero to prevent the economy from collapsing. It worked, but it also meant that savers earned very little on their deposits for years. Now, as inflation has been creeping up, the Fed has been raising rates to keep things in check. It’s all about maintaining stability and preventing economic chaos.

Impact on Inflation

Inflation is like the Fed’s arch-nemesis. When prices start rising too fast, the Fed uses its rate-setting powers to bring things back to normal. By hiking rates, it makes borrowing more expensive, which reduces spending and slows down price increases. It’s a bit like putting the brakes on a runaway train.

But here’s the catch: raising rates too quickly can backfire. If businesses and consumers cut back too much, it can lead to a slowdown or even a recession. That’s why the Fed has to tread carefully when adjusting rates. It’s a high-wire act that requires precision and foresight.

Historical Context of Fed Rates

To truly understand fed rates, it helps to look at their history. Back in the 1970s, the U.S. experienced runaway inflation, with prices skyrocketing and the economy in turmoil. The Fed had to take drastic measures, hiking rates to double-digit levels to bring things under control. It worked, but it also caused a deep recession.

In recent years, fed rates have been relatively low, especially after the 2008 financial crisis. The Fed kept rates near-zero for years to help the economy recover. But as the economy strengthened and inflation picked up, the Fed began gradually raising rates again. It’s a cycle that repeats itself, and understanding it can help you make smarter financial decisions.

Key Moments in Fed Rate History

- 1980s: Double-digit rates to fight inflation

- 2008: Near-zero rates during the Great Recession

- 2022: Rate hikes to combat rising inflation

These moments highlight the Fed’s role as the economy’s guardian. It’s always on the lookout for signs of trouble and ready to act when necessary. Whether it’s raising rates to cool down inflation or cutting them to jumpstart growth, the Fed’s decisions have far-reaching consequences.

How Fed Rates Impact Borrowing

If you’re in the market for a loan, fed rates are your new best friend—or your worst enemy, depending on how you look at it. When rates are low, borrowing is a breeze. Mortgages, car loans, and personal loans all come with lower interest rates, making them more affordable. But when rates rise, those same loans can become a financial burden.

For example, if you’re shopping for a home and the Fed raises rates, your mortgage payments could go up significantly. That’s because most mortgages are tied to the prime rate, which is influenced by fed rates. So, if you’re planning a big purchase, timing is everything. Keeping an eye on fed rates can help you make the most of your borrowing opportunities.

Impact on Credit Cards

Credit cards are another area where fed rates have a big impact. Most credit cards have variable interest rates that are tied to the prime rate. When the Fed raises rates, your credit card APR goes up too. That means if you carry a balance, you’ll end up paying more in interest. It’s a good reminder to pay off your credit card bills in full whenever possible.

But here’s a silver lining: some credit card issuers offer promotional rates or balance transfer deals when rates are low. If you’re strategic, you can take advantage of these offers to save money on interest. Just make sure you read the fine print and pay off the balance before the promotional period ends.

Fed Rates and the Stock Market

Now, let’s talk about the stock market. Fed rates have a big influence on how stocks perform. When rates are low, companies can borrow money more easily to invest in growth, which can boost stock prices. But when rates rise, borrowing becomes more expensive, which can weigh on corporate profits and drag down stock prices.

Investors pay close attention to fed rate decisions because they can signal where the economy is headed. If the Fed raises rates, it might mean the economy is strong, which is generally good news for stocks. But if rates go up too fast, it could signal that the Fed is worried about inflation, which might spook investors and lead to market volatility.

How Investors React to Fed Rate Changes

Investor reactions to fed rate changes can be unpredictable. Some might see rate hikes as a sign of economic strength and buy more stocks. Others might worry about the impact on corporate profits and sell off their holdings. It’s a rollercoaster ride that keeps financial analysts on their toes.

One thing’s for sure: staying informed about fed rates can give you an edge as an investor. By understanding how rate changes affect different sectors of the market, you can make more informed decisions about where to put your money.

Fed Rates and Global Markets

Fed rates don’t just affect the U.S. economy—they have ripple effects around the world. When the Fed raises rates, it can strengthen the dollar, making it more attractive to foreign investors. But it can also make it harder for other countries to repay their dollar-denominated debts, leading to financial instability in some regions.

Emerging markets, in particular, are vulnerable to fed rate changes. A stronger dollar can make their currencies weaker, which can hurt their economies. That’s why global markets keep a close eye on what the Fed is doing. It’s all interconnected, and a small change in fed rates can have big consequences worldwide.

Impact on Currency Markets

Currency traders are especially attuned to fed rate changes because they can cause significant movements in exchange rates. When the Fed raises rates, the dollar tends to strengthen, which can affect everything from trade balances to tourism. For example, a stronger dollar makes U.S. exports more expensive, which can hurt American businesses that rely on foreign sales.

But a stronger dollar can also be a boon for travelers and importers. If you’re planning a trip abroad, a strong dollar means your money will go further. And if you’re buying goods from overseas, you might get a better deal. It’s all about finding the right opportunities in a changing currency landscape.

Fed Rates and Personal Finance

Let’s bring it back to you, the everyday consumer. Fed rates affect your personal finances in more ways than you might realize. From your savings account to your credit card bills, every financial decision you make is influenced by what the Fed does. So, how can you make the most of it?

First, stay informed. Keep an eye on fed rate announcements and adjust your financial strategies accordingly. If rates are rising, consider locking in fixed-rate loans before they get too expensive. If rates are low, it might be a good time to refinance your mortgage or take out a new loan. Being proactive can save you a lot of money in the long run.

Tips for Managing Your Finances in a Changing Rate Environment

- Refinance high-interest debt when rates are low

- Lock in fixed-rate loans before rates rise

- Shop around for the best savings account rates

- Pay off credit card balances to avoid higher interest charges

These tips can help you navigate the ups and downs of fed rates and keep your finances on track. Remember, knowledge is power, and staying informed is the key to financial success.

Conclusion: Why Fed Rates Matter to You

So, there you have it. Fed rates might seem like a dry, technical topic, but they have a huge impact on your everyday life. From your mortgage payments to your credit card bills, every financial decision you make is influenced by what the Fed does. By understanding how fed rates work and how they affect the economy, you can make smarter financial choices and protect your wallet.

Here’s the bottom line: don’t underestimate the power of fed rates. They’re a key driver of the economy, and they can make or break your financial future. So, stay informed, stay proactive, and don’t be afraid to ask questions. Your financial well-being depends on it.

Now, it’s your turn. Do you have any questions about fed rates? Or maybe you’ve got a story about how they’ve affected your finances. Drop a comment below and let’s keep the conversation going. And if you found this article helpful, don’t forget to share it with your friends and family. Knowledge is power, and the more we know, the better off we’ll be.

Table of Contents:

- What Exactly Are Fed Rates?

- Why Should You Care About Fed Rates?

- How Do Fed Rates Affect the Economy?

- Historical Context of Fed Rates

- How Fed Rates Impact Borrowing

- Fed Rates and the Stock Market

- Fed Rates and Global Markets

- Fed Rates and Personal Finance

- Conclusion: Why Fed Rates Matter to You

Eugene Henley: The Untold Story Of A Visionary Entrepreneur And Innovator

Jaden McDaniels: The Rising Star In The NBA

Fed Interest Rates: The Game Changer In Global Economy

Fed Rates 2025 Imran Faye

Fed Interest Rates 2024 July Vanni Orsola

Fed Rates May 2024 Natty Viviana