Fed Rates: A Deep Dive Into How They Impact Your Wallet And The Economy

When it comes to understanding the economy, the term "Fed Rates" is like the holy grail of financial jargon. But don’t let that scare you—it’s not as complicated as it sounds. Think of it this way: the Federal Reserve, aka the Fed, is like the conductor of the U.S. economy’s orchestra. And their main instrument? You guessed it—Fed Rates. These rates are essentially the interest rates banks charge each other for borrowing money overnight. Yeah, I know—it sounds super boring on paper, but trust me, it’s a big deal.

Now, you might be wondering, "Why should I care about some fancy financial terms?" Well, here’s the kicker: Fed Rates affect everything from your mortgage payments to your credit card interest. That means they’ve got a direct line to your wallet. So, whether you’re saving for a dream house or just trying to pay off student loans, knowing how Fed Rates work can make a huge difference in your financial journey.

Before we dive deep into the nitty-gritty, let’s clear the air: this ain’t just about numbers and graphs. It’s about YOU. It’s about understanding how decisions made by a bunch of economists in Washington can impact your daily life. So buckle up, because we’re about to break it down in a way that even your non-finance-savvy friends can get behind.

What Are Fed Rates, Anyway?

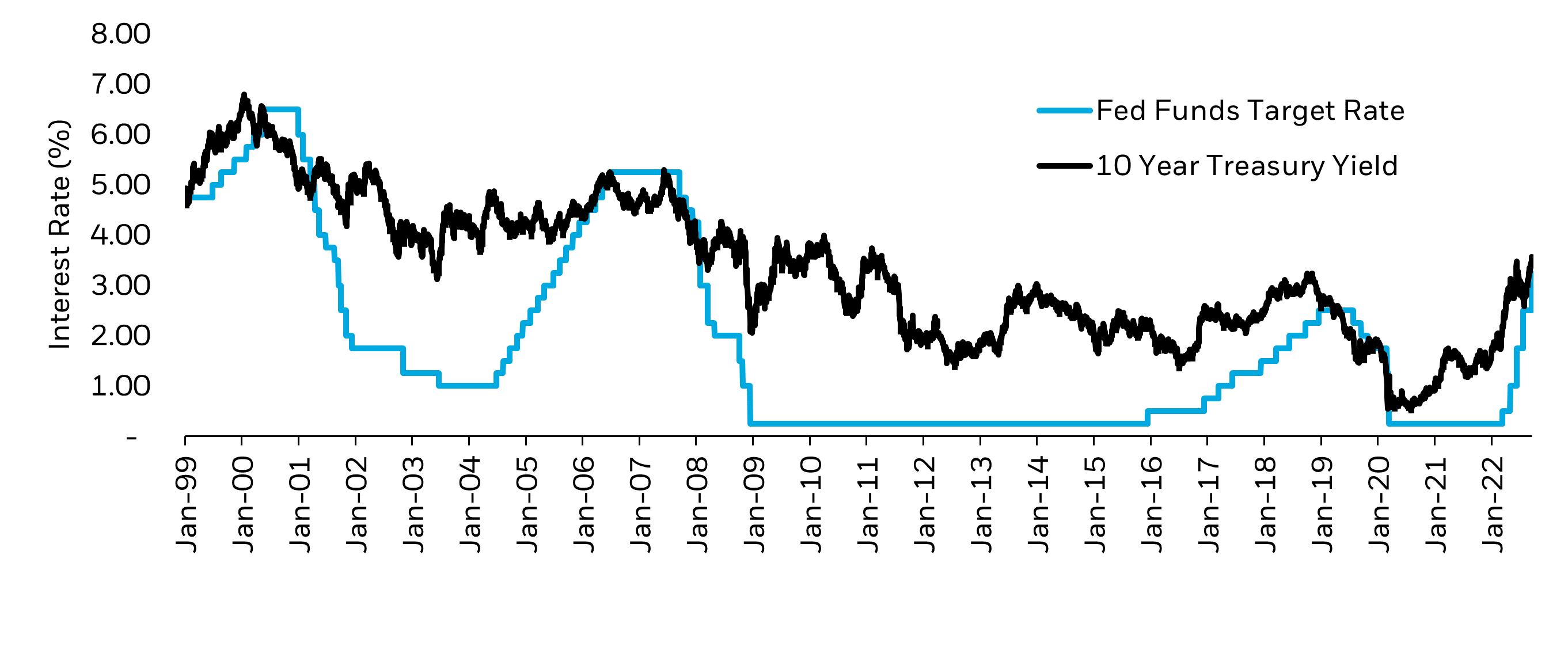

Let’s start with the basics. Fed Rates, or the Federal Funds Rate, is the interest rate at which banks lend money to each other overnight. Think of it as a bank’s version of a payday loan, but way more legit. The Fed uses this rate as a tool to control inflation and keep the economy on track. When the economy’s running hot, they might raise the rates to cool things down. On the flip side, if things are sluggish, they’ll lower the rates to give it a boost.

Here’s the thing: Fed Rates aren’t just some random number the Fed pulls out of thin air. They’re set by the Federal Open Market Committee (FOMC), which meets eight times a year to decide what the rates should be. It’s like a big financial summit where all the bigwigs sit around a table and hash it out. And trust me, these meetings can get pretty intense.

Why Do Fed Rates Matter to You?

Alright, so you’ve got a basic idea of what Fed Rates are, but why should you care? Here’s the deal: when the Fed adjusts these rates, it sets off a chain reaction that affects pretty much every aspect of the economy. Let me break it down for you:

- Mortgage Rates: When Fed Rates go up, mortgage rates tend to follow suit. That means if you’re thinking about buying a house, you might end up paying more in interest.

- Credit Card Interest: Same deal here. Higher Fed Rates usually mean higher credit card interest rates. So if you’re carrying a balance, you might want to pay it off sooner rather than later.

- Savings Accounts: On the flip side, when rates go up, you might see better returns on your savings accounts. It’s like a little silver lining in an otherwise stormy financial sky.

So yeah, Fed Rates might seem like this distant financial concept, but they’ve got a direct line to your wallet. And understanding how they work can help you make smarter financial decisions.

How Do Fed Rates Impact the Economy?

Now that we’ve covered the personal impact, let’s zoom out and look at the bigger picture. Fed Rates play a crucial role in shaping the overall economy. When the rates are low, borrowing becomes cheaper, which encourages businesses to invest and consumers to spend. This can lead to job creation and economic growth. On the other hand, when rates are high, borrowing becomes more expensive, which can slow down the economy and reduce inflation.

But here’s the tricky part: the Fed has to strike a delicate balance. If they keep rates too low for too long, it can lead to inflation spiraling out of control. And if they raise rates too quickly, it can stifle economic growth and even lead to a recession. It’s like walking a tightrope, and the Fed has to be super careful not to fall off either side.

The Fed’s Dual Mandate

Speaking of balance, the Fed has what’s called a "dual mandate." Their job is to promote maximum employment and keep prices stable. It’s like having two bosses with sometimes conflicting demands. On one hand, they want to make sure as many people as possible have jobs. On the other hand, they need to keep inflation in check so that prices don’t skyrocket.

This dual mandate is why the Fed pays so much attention to economic indicators like unemployment rates and inflation. They use this data to make informed decisions about where to set Fed Rates. And let me tell you, it’s not an easy job. They’ve got to weigh a lot of factors and make some tough calls.

Historical Context: A Look Back at Fed Rates

To really understand how Fed Rates work, it helps to look at some historical context. Over the years, the Fed has adjusted rates in response to various economic conditions. For example, during the 2008 financial crisis, they dropped rates to near zero to stimulate the economy. And in the late 1970s and early 1980s, they raised rates dramatically to combat runaway inflation.

One of the most famous examples of Fed Rate adjustments is the Volcker Shock of the early 1980s. Under Chairman Paul Volcker, the Fed raised rates to over 20% to bring inflation under control. It was a painful but necessary move that helped stabilize the economy in the long run. And while it caused a lot of short-term pain, it ultimately set the stage for years of economic growth.

Key Moments in Fed Rate History

- 1970s Inflation: The Fed struggled to control inflation, leading to double-digit interest rates.

- 2008 Financial Crisis: Rates were slashed to near zero to prevent a total economic collapse.

- 2020 Pandemic: The Fed once again dropped rates to near zero to help the economy weather the storm of the global pandemic.

These historical examples show just how powerful Fed Rates can be in shaping the economy. And they also highlight the challenges the Fed faces in making the right decisions at the right time.

How Are Fed Rates Determined?

So how exactly does the Fed decide what the rates should be? It’s not as simple as flipping a coin or pulling a number out of a hat. The FOMC uses a variety of economic indicators to make their decisions. They look at things like:

- Inflation: If inflation is too high, they might raise rates to cool things down.

- Unemployment: High unemployment might prompt them to lower rates to stimulate job growth.

- GDP Growth: If the economy’s growing too fast, they might raise rates to prevent overheating.

It’s a complex process that involves a lot of data analysis and forecasting. And while the FOMC tries to be as transparent as possible, their decisions can sometimes be a bit unpredictable. After all, they’re dealing with a constantly changing economic landscape.

The Global Impact of Fed Rates

While we’ve been focusing on the U.S. economy, it’s important to note that Fed Rates have a global impact as well. Because the U.S. dollar is the world’s reserve currency, changes in Fed Rates can affect economies all over the world. For example, when the Fed raises rates, it can lead to capital flowing out of emerging markets and back into the U.S. This can cause currency fluctuations and economic instability in other countries.

So yeah, the Fed’s decisions don’t just affect Americans—they’ve got global implications. And that’s why central banks around the world keep a close eye on what the Fed is doing. It’s like a giant game of financial chess, and the Fed is one of the key players.

How Other Countries Respond to Fed Rate Changes

When the Fed adjusts rates, other countries have to decide how to respond. Some might follow suit and adjust their own rates, while others might take a different approach. It all depends on their economic situation and how they think the Fed’s actions will affect them. And let me tell you, it’s not always a straightforward decision.

This global interconnectedness is why the Fed’s decisions are so closely watched by economists and policymakers around the world. It’s not just about the U.S. economy—it’s about the global economy as a whole.

Understanding the Fed’s Role in the Economy

Now that we’ve covered the ins and outs of Fed Rates, let’s take a step back and look at the Fed’s role in the economy as a whole. The Fed is like the quarterback of the U.S. economy, calling the plays and making sure everything runs smoothly. But unlike a football team, the Fed doesn’t have the luxury of timeouts or halftime adjustments. They’ve got to be constantly vigilant and ready to make changes at a moment’s notice.

And while they’ve got a lot of tools at their disposal, Fed Rates are one of their most powerful weapons. By adjusting these rates, they can influence everything from inflation to unemployment to economic growth. It’s a big responsibility, and one that they take very seriously.

How Can You Protect Yourself from Fed Rate Changes?

So now that you know how Fed Rates work, how can you protect yourself from their effects? Here are a few tips:

- Pay Down Debt: If you’ve got high-interest debt, try to pay it off before rates go up.

- Lock in Low Rates: If you’re planning to buy a house or take out a loan, consider locking in a low rate while you can.

- Invest Wisely: When rates are low, it might be a good time to invest in stocks or real estate. But be cautious when rates start to rise.

Ultimately, the key is to stay informed and make smart financial decisions. The more you understand how Fed Rates work, the better equipped you’ll be to navigate the ever-changing economic landscape.

Conclusion: Take Control of Your Financial Future

So there you have it—a deep dive into the world of Fed Rates. From their impact on your wallet to their role in shaping the global economy, these rates are a powerful force that affects us all. And while they might seem like this distant financial concept, understanding how they work can help you make smarter financial decisions.

So the next time you hear about the Fed adjusting rates, don’t just tune it out. Pay attention, because it could affect your financial future. And if you’ve got any questions or thoughts, drop them in the comments below. We’d love to hear from you!

Table of Contents

Why Do Fed Rates Matter to You?

How Do Fed Rates Impact the Economy?

Historical Context: A Look Back at Fed Rates

The Global Impact of Fed Rates

How Other Countries Respond to Fed Rate Changes

Understanding the Fed’s Role in the Economy

How Can You Protect Yourself from Fed Rate Changes?

More AKUS 2025 Tour News – Stuart Duncan Added, TV March 19

Jackie Robinson Article: The Untold Story Of His Army History And Its Restoration To The DoD Website

Cavaliers Vs Kings Prediction, Picks & Odds For Tonight’s NBA Game

Fed Rates 2025 Imran Faye

Fed Interest Rates 2024 July Vanni Orsola

Fed Rates May 2024 Natty Viviana